The $2T Compute Financing Middle Market

A $2T compute-backed lending opportunity overlooked by traditional capital providers.

July 9, 2026

Written by Conor Moore, COO and Co-Founder of Permian Labs, developer of USD.AI. Originally published on July 8, 2026.

SemiAnalysis published an excellent map of the GPU financing market this week. But one of the most compelling areas of this sector today was relegated to a single call out on a chart, labeled “highest credit risk”, and given no further thought: the compute middle market.

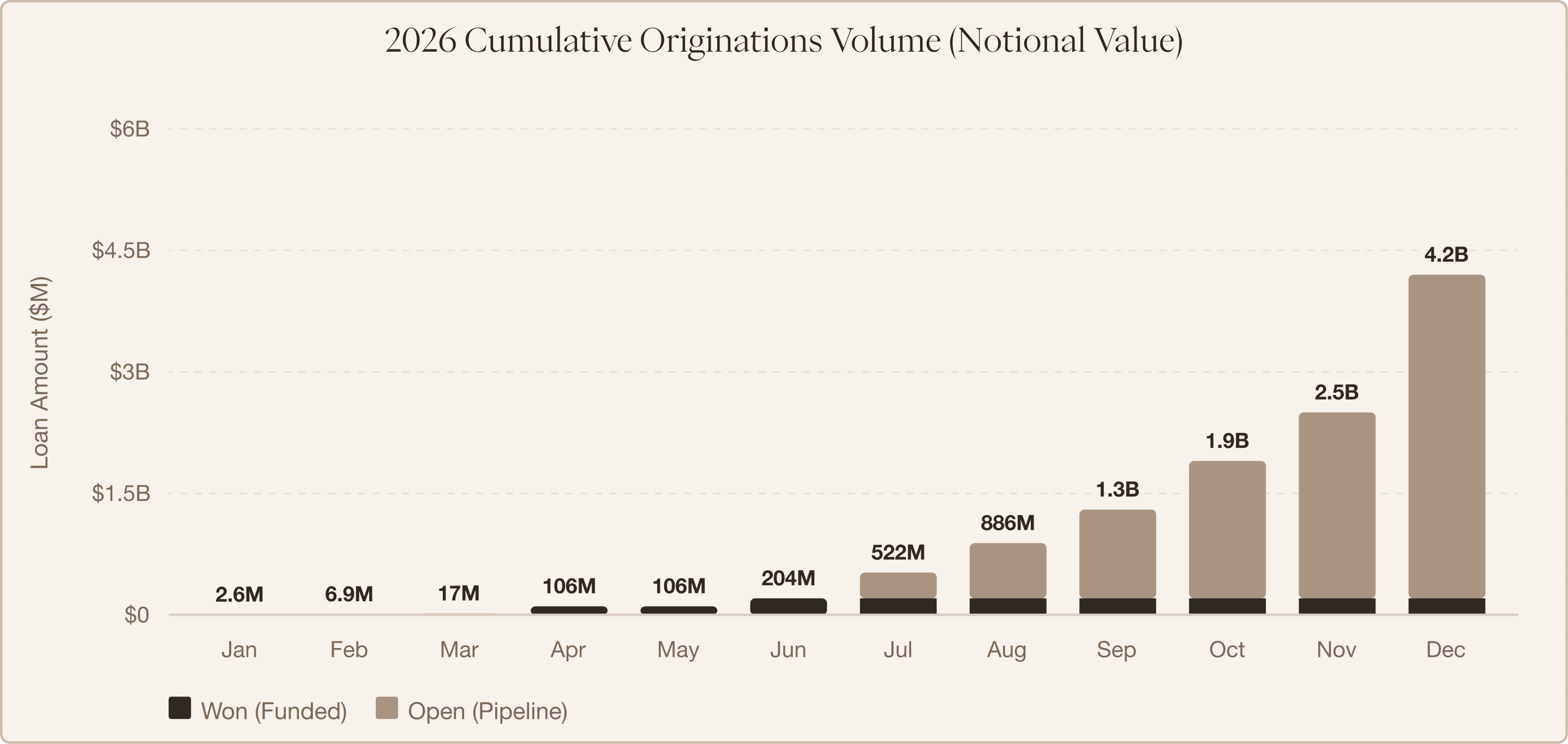

Over the last 8 months, USD.AI has seen $13bn in deals across 200+ neoclouds in exactly this segment, which we estimate at $2T in spend through 2030. Properly structured and with synthetic credit enhancements (more on this below), middle market compute financings deliver the same security package and credit profile as IG backstopped deals, with 400 to 600 basis points of additional yield. We think it is the best risk adjusted return in asset backed finance today.

Over the last 8 months, USD.AI has seen $13bn in deals across 200+ neoclouds in exactly this segment, which we estimate at $2T in spend through 2030. Properly structured and with synthetic credit enhancements (more on this below), middle market compute financings deliver the same security package and credit profile as IG backstopped deals, with 400 to 600 basis points of additional yield. We think it is the best risk adjusted return in asset backed finance today.

The Compute Market Segments

-

Hyperscale ($2bn+) – syndicated debt capital markets. These are not GPU financings at all. They are corporate financings by Microsoft, Meta and Oracle where the proceeds happen to buy GPUs, and they are priced as such.

-

Large scale ($250m - $2bn) – private credit sweet spot. Underwriting rests on IG offtakes and parent guarantees. Funds backlever a mid single digit IRR into a low double digit one to hit a hurdle. This is a straightforward IG arb.

-

Middle market ($50m - $250m) – few capital providers, lots of borrower demand, fundamentally misunderstood industry subsector.

-

Micro clusters (sub $50m) – financed by equipment lessors. Hard assets are the total collateral package. 25%+ IRRs with a full repo-and-resale operation built in house and diversification across counterparties.

The middle market is the only segment where the lender has to understand the full compute stack to participate. Large scale and hyperscale are just corporate IG financings, while micro scale is just another equipment lease no different from a tractor or hospital bed.

This is clearer with NVIDIA’s new backstop initiative. As SemiAnalysis says, most lenders “still hide behind the shield of an investment grade offtake or backstop”. If NVIDIA wants to sell GPUs to more than just hyperscalers, they have to substitute their own IG rating in place of the hyperscaler’s. But this is not the only way to synthetically improve credit risk, nor is it the most cost effective.

As a whole, we believe the credit risk of the compute middle market is heavily mispriced, for a number of reasons.

Why Middle Market Compute Credit Is Mispriced

-

0 days of speculation (“last mile” financing): middle market clusters (1-10 MW) are deployed into existing colocation facilities and permanent financing is only released upon installation. The size of the cluster allows for deployment into leftover colo space and enables OEMs to be more comfortable granting net payment terms. This is in stark contrast to gigawatt datacenter deployments, which require 24-36 month speculative construction timelines. A GPU to be deployed is a fundamentally different asset from one that is already deployed.

-

Structural parity with IG deals: We structure deals with the following: (1) Bankruptcy remote SPV with an independent manager, (2) Customer contracts assigned to the SPV, with SPV level bank accounts under a DACA, (3) First priority charge over the GPUs plus a pledge of the SPV equity, perfected by UCC-1 filing, (4) Step-in rights to the colocation facility via an MSA lien waiver, including the right to sell servers in an EOD, (5) Debt service reserve account funded upfront with 1 to 3 months of P&I; rent collections top up the DSRA before anything releases to the parent. Lenders do not need to give up any structural protections to win deals in the middle market, borrowers are sophisticated operators who can navigate traditional loan and security packages.

-

Conservative LTC detachment point: Sponsors put 20-30% cash down plus 1-3 months of reserved debt service, creating effective buffers of up to 40% of total asset value. Many of the IG backstopped deals are effectively 100% debt financed. The equity check size also acts as a filter, screening out poorly capitalized / upstart operators.

-

Contracted cashflows with real tenor: SemiAnalysis reports that inference providers are unwilling to sign beyond one year. In the middle market, we most commonly see 3 to 4 year take-or-pay leases signed by inference providers and non-US hyperscalers, generally matched to the tenor of the loan.

-

Value insurance to create synthetic IG backstop: In the event of default, a lender can simply capture the delta between the insured value and recouped value. The insurance is sourced from IG rated carriers, effectively getting the same contractual protections and credit support as provided by an IG offtaker.

Altogether, the credit profile of these deals, through separate enhancements and structural protections, closely resembles that of hyperscaler backed deals, but at net coupons 400 to 600 bps higher. The opportunity exists not based on some directional risk taking, but rather an educational gap between those who know compute, and those with the capital to deploy. Institutional rigidity and bureaucracy in the banking system have left a $2T financing need unmet. For which we are extremely grateful.

USD.AI deploys capital programmatically and from first principles. The data drove us to the compute middle market, not any prescriptive thesis about what the future of compute can or should look like. If you want to see the opportunity set for yourself, please reach out to hello@usd.ai.

Disclaimer: This article reflects the personal views of the author and is shared for informational purposes only. It does not necessarily represent the official position of Permian Labs or USD.AI, and should not be interpreted as financial, investment, legal, or tax advice.